Finance & investing

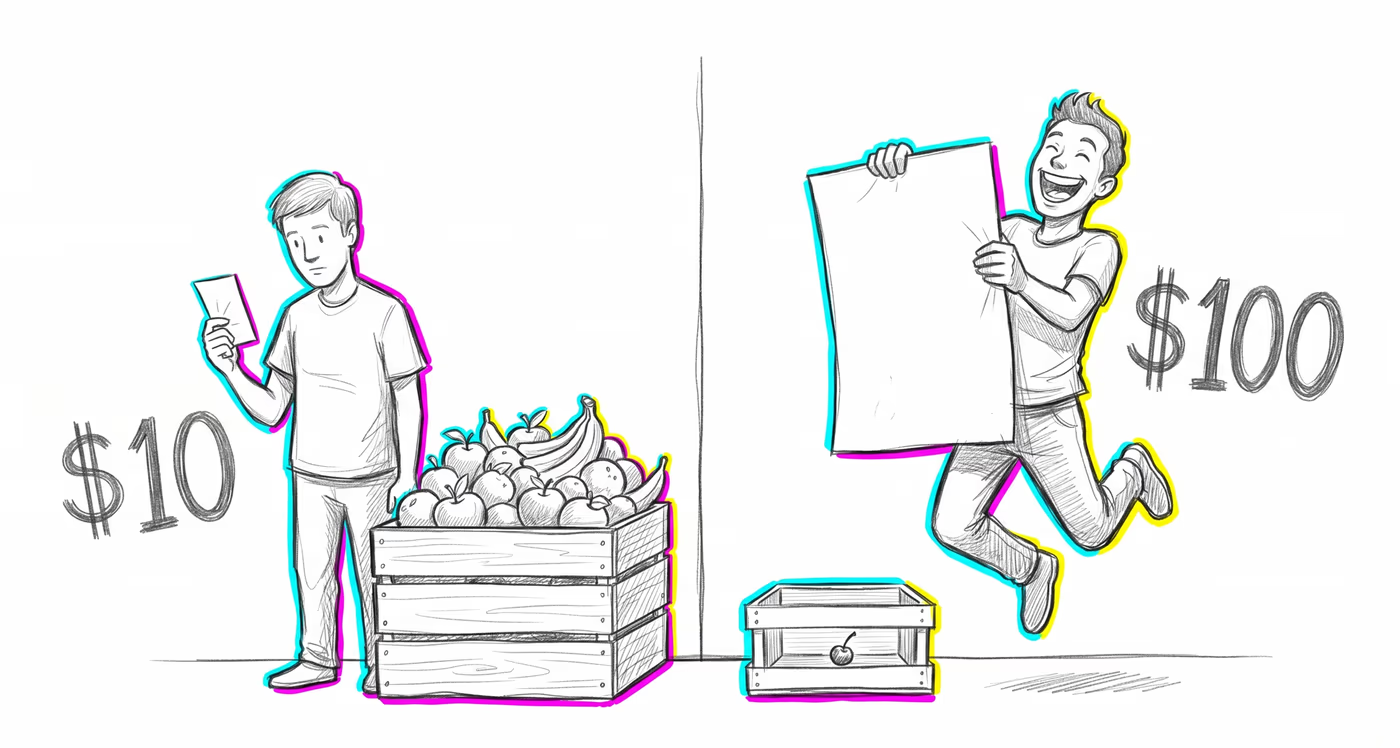

Investors often segregate portfolios into 'safe money' and 'play money' buckets, taking excessive risks with gains or windfalls while being overly conservative with principal. This leads to suboptimal asset allocation because risk and return are evaluated per-account rather than across the total portfolio.