Finance & investing

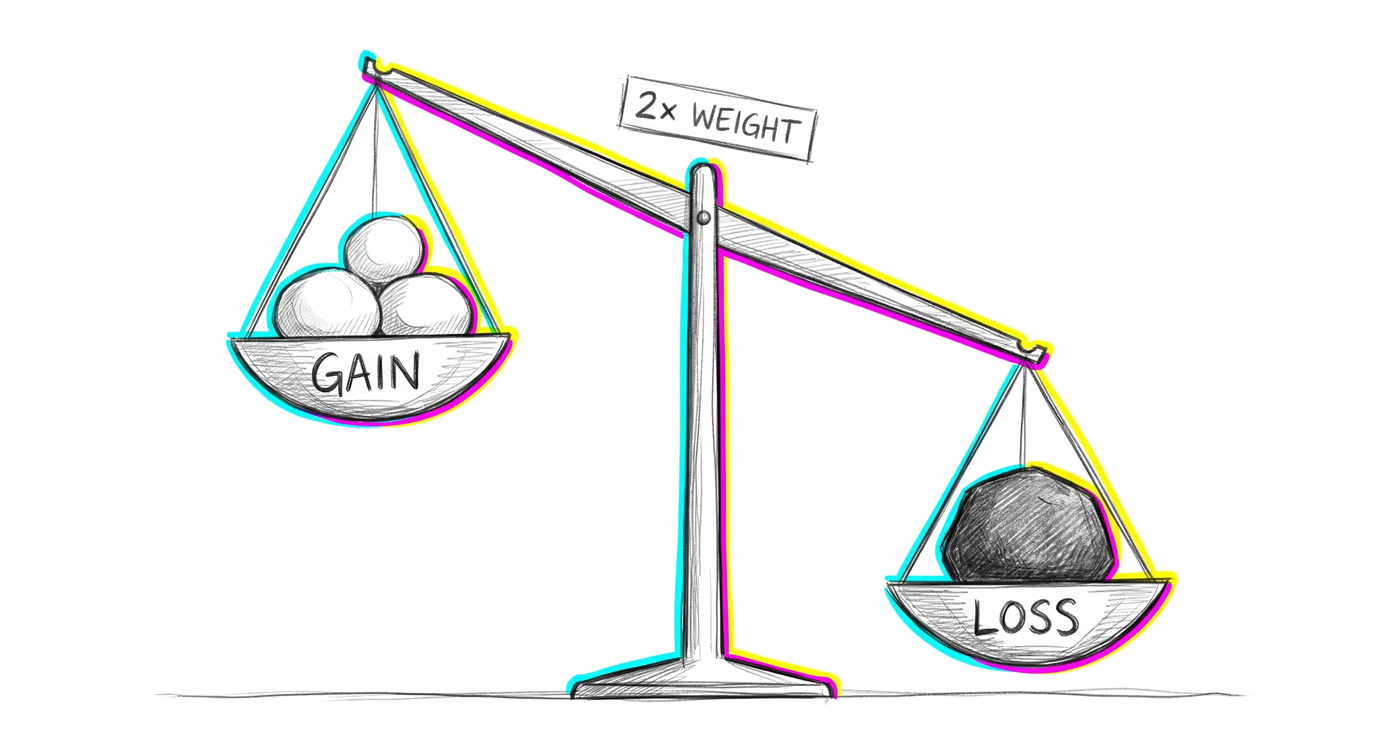

Investors and consumers systematically under-save for retirement, prefer lump-sum payouts over annuities with higher total value, carry high-interest credit card debt while holding low-yield savings, and cash out investment positions prematurely rather than allowing compound growth to accumulate over time.